N.B.: This was originally a lecture for the NationStates World Fair III. I wanted to make it more widely available, so I am posting it here.

I’m an economist by training and by hobby, so I thought that for the purpose of my lecture I’d stick with something I know about. The lecture’s title is actually somewhat misleading, because I’m not trying to push realism on any player. One thing that makes NationStates so great is the fact that we can essentially roleplay however we damn please — whoever doesn’t like it can roleplay with someone else. At the same time, I know that there are a lot of people interested in realism, or would at least like to be informed by realism, so this lecture really serves as a guide and using it as such is completely up to you.

Also, I will try to minimize discussion of theory. My intention is merely to provide interesting facts about the organization of international trade patterns. I’ll link to more detailed theoretical discussions when proper, and you can click-through if you’d like.

What do I mean by trade?

This is not about storefronts and instead applies to the trade we tend to think less about. What I mean by that is, for example, the imports, exports, and trade partners we list on our factbooks. I think the term “free trade” captures this well, because it’s the kind of trade that is determined by millions of individual actors who use local knowledge to figure out how much of a foreign product they need to purchase and how much of their product they can sell internationally. Storefronts, for the purpose of this lecture, is closer to “centrally planned trade,” since this is trade we push regardless of what economics says (because having fun > super strict realism).

Similarly, this lecture doesn’t concern those countries that have their trade patterns determined entirely by their governments, or centrally planned economies. In these cases, trade patterns are more determined by political relationships, bilateral trade agreements, quotas, and export subsidies. Economic theory isn’t totally silent on this, but the gist of what trade theory has to say in these situations is that your trade balances are going to be incredibly constrained, in a negative sense (for a real-life example, look at German interwar imports and exports after 19341).

Neither do the arguments in this lecture apply to post-scarcity economies. In a post-scarcity world, all wants are, by definition, satisfied. As such, the incentive to trade is completely eliminated. Put more directly, in a post-scarcity world there would be no trade at all. I personally do not believe that a post-scarcity world is possible, since I believe human wants are limitless (and predictors of post-scarcity have been constantly proved wrong), but this is a discussion for another day — and, again, it’s your country, so do as you please!

Some Empirical Observations2

Empirically, we can predict trade volumes between countries based on the following formula, which I will fully explain:

Tij = A × Yi × Yj/Dij

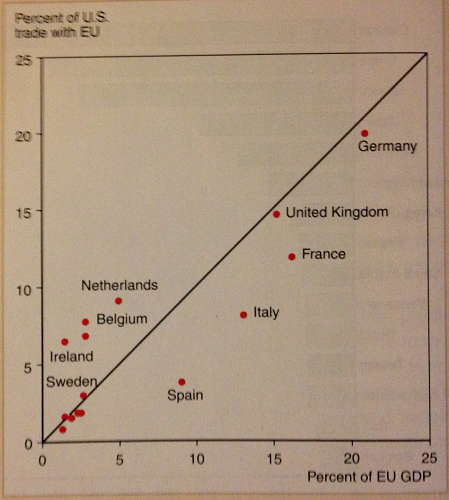

This is known as the “Gravity Model.” Regarding the variables, don’t worry about A, as it’s just a constant. The important part of the model is that it’s basically saying that Trade between countries i and j is determined by the combined sizes of both countries gross domestic output (GDP; also referred to as output or national income), divided by the distance between the two countries. In other words, the two main empirical determinants of trade between two nations are the relative sizes of their economies and the distance between them.

Here we see an illustration of how relative sizes of economies determines trade (sorry for the horrible quality, had to use my camera phone):

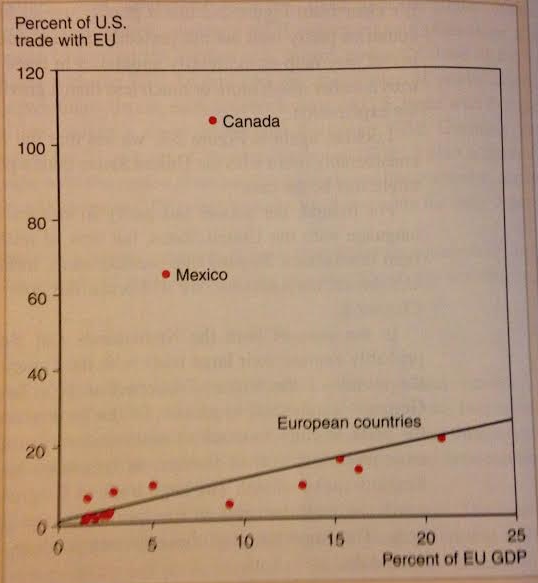

Now, here’s an empirical illustration about the influence distance — a good proxy for the costs to trade — has on trade volume:

As you can see, while Mexico and Canada may not compare to other countries in GDP size, they are very close to the United States. That drastic reduction in distance plays such a large role that despite the dramatic differences in GDP, Mexico and Canada still trade much more with the United States than any other nation.

So, how does this translate to NationStates? Let’s use a map of Greater Díenstad as an example, to provide context. For GDP sizes, let’s use a calculator.

Let’s take my country, The Macabees — the largest economy in the region, according to the above-linked calculator —, and go through the logic of who I’d trade with the most. For the sake of simplicity, let’s assume away all tariffs, quotas, subsidies, and preferential trade agreements — in other words, assume the entire region practices free trade.

My largest trade partner is most likely Stevid, because not only is his economy large (the second largest in Greater Díenstad), but he’s also a neighbor. This case is pretty straightforward, so let’s take a less obvious example. You won’t find Safehaven on a calculator, because he CTEd a long time ago, but its economy is very, very poor (Safehaven is a failed state). Countries like Morrdh, Mokastana, and Haishan have larger GDPs than Safehaven, yet, because Safehaven is right next to me and the other three countries are on the other side of the map, we can safely predict that trade volume between The Macabees and Safehaven will be greater than trade volumes between The Macabees and any of the other three. I’d also expect greater trade volume between Safehaven and I than between United Gordonopia and I, even though Gordonopia has a larger GDP than Safehaven.

In summary, in overall terms trade volumes between your country and other countries should be mainly determined by two things: how similar in size the other country’s economy is to yours (large economies tend to trade less with small economies than they do with other large economies) and how close the other country is to yours.

- The smaller or larger the other economy is compared to yours, the less you will trade with it.

- The farther away the other economy is to yours, the less you will trade it.

Which Goods are Traded with Whom (Wonkish)?

If you’ve taken an Economics 101 course, you’ve probably been taught comparative advantage. According to the theory of comparative advantage, each country trades in what it has a comparative advantage is. In English: each country trades in what it can produce at the lowest cost, compared to every other trade partner. The theory’s strict prediction is that each country will export only those goods it specializes in and will import only those goods it’s less efficient at producing. As it turns out, this theory doesn’t fit reality very well.

Fortunately, the theory of comparative advantage has been well complemented by a more recent contribution to trade theory: the role of economies of scale. I might have to bore you a little, but I’ll hold back on the theoretical discussion as much as possible. For a more complete, but still popular, account of the theory of economies of scale and trade see: “Krugman’s Alternative Theory of Trade” (sorry about the slow loading time, I’m working on that).

Economies of scale occur when an increase in output leads to falling average unit costs of production. In the context of a firm, we usually see economies of scale when there are high fixed costs — high overhead, in a sense. In these cases, the reason we see economies of scale is because those fixed costs are spread over a larger number of goods. Another rationale behind economies of scale within a firm is increased specialization amongst employees, and this logic caries forward to the economy in general (i.e. the division of labor). Economies of scale matter because as an economy increases output average unit costs fall, and therefore the goods in question become more competitive internationally. Above, I mentioned that a country will be a net exporter in goods it has the larger market for (compared to other countries); that's because the greater demand allows it to exploit greater economies of scale, and therefore relevant firms can export the good at a lower price than firms from other countries.

What’s so attractive about this trade theory is that it does a better job of explaining real world trade than just old fashioned comparative advantage theory. The conclusions we can take from the theory include:

- Because transportation costs are positive, these are barriers to specialization. The greater the transportation costs (the greater the distance), the less specialized each country will be in its imports and exports. In other words, what we’d see more of us international intra-industry trade. A good real world example is the auto industry: American vehicles are exported to Europe, and European vehicles are exported to the United States.

- Larger populations make for wealthier countries, since the opportunity for economies of scale is greater. Furthermore, larger populations tend to attract immigrants because real wages are higher (the number of goods you can buy with the same wage is greater). And the more immigrants, the larger your population, the higher your real wages. As barriers to trade fall, this becomes less true, since costs to trade can’t stop different populations from integrating. Edit: Real wages are higher, because a larger population allows for greater economies of scale, which will lower average unit costs (i.e. prices).

- Because of positive costs to trade, local demand will for the most part determine economies of scale, so the good where domestic demand is highest will also be the good more likely to be exported, all else equal.

- In a carry-over from the theory of comparative advantage, the more unique your factors of production (e.g. suppose you’re the only country that produces zinc and has zinc as a factor of production), the more likely you are to export goods that are intensive in that factor of production. The more uniform factors of production are between countries, the more likely intra-industry trade becomes.

Because on NationStates we tend to have many of the same factors of production, intra-industry trade is more likely than the specialized trade predicted by comparative advantage. Furthermore, because of the significant distances involved in international trade, most of the time, the forces that promote intra-industry trade are even greater. What this means is that if you export oil, then you’re likely to import oil as well. Likewise, if you export tractors, you’re also likely to import tractors.

Finally, how do we know what good your country is a net exporter in and a net importer in? All else equal, countries will be net exporters in goods where home demand is largest relative to other economies. So, if your country has a greater demand for wine than any other country, all else equal you are likely to be a net exporter in wine.

Quality of Goods Traded

This will be a short section, just to explain why, as distances grow, the average quality of the goods being traded will increase. The Alchian-Allen Theorem applies when we’re talking about intra-industry trade. Suppose that Lamoni produces both high-grade and low-grade orange, with the prices of $8 and $6, respectively. Let’s first assume that shipping costs are free, so the relative cost of high-grade oranges is ~1.3. But, now let’s assume that shipping costs are $1 per orange, such that the prices for both goods are boosted to $9 and $7, respectively. Now, the relative price is 1.29, so the relative demand for the higher-priced orange increases in Lyras. In other words, relatively speaking, the cost of high-quality Lamonian oranges has decreased for Lyrans.

Another lesson the Alchian-Allen Theorem teaches us is very highly priced goods are more likely to be sold internationally than they are likely to be sold to domestic markets. Suppose California produces two-grades of beer, one valued at $6 and the other at $3. In California, the relative cost of high-grade beer will be 2, but in Florida the relative cost will also be informed by a shipping cost greater than zero. Say that shipping cost is $2, the relative cost of high-quality beer for Floridans is 1.6. Thus, high-quality Californian beer (according to this example) may sell more in Florida than it does in California.

The Economics of FutureTech Roleplay (Wonkish)

Because human involvement in space is limited in real life, there hasn’t been much written on the economics of inter-planetary trade. There are a few exceptions, which include Paul Krugman’s “The Theory of Interstellar Trade,” Espen Haug’s “Space-time Finance,” and John Hickman’s “Problems of Interplanetary and Interstellar Trade.” For not-so-dry reading, you can also peruse economist Noah Smith’s list of “Science Fiction Novels for Economists.”

My knowledge in this area is quite limited. Some basic principles to remember is that in a world without faster-than-light (FTL) travel, interplanetary trade will be quite limited and we would probably see something similar to what markets looked on Earth prior to the globalization that has taken place since the 17th century. In other words, fragmented, but indirectly interconnected via intermediary economies (e.g. the Middle Eastern economy enjoyed quite a bit of income as an intermediary between Europe and China).

The real interesting stuff happens when we assume FTL or near-FTL, because the nature of time changes. In Earth-bound trade, the differences in relative time are so minute that they can be ignored. But, in interstellar trade relative time plays a significant economic role. Consider the rate of interest, which is the ratio between the value of some set of goods now and the value of the same set of goods in the future (time preference). Another way of defining the rate of interest is the value of the merchant’s cargo upon arrival at her destination. The difficulty lies in figuring out the rate of interest, since, in near-FTL or FTL travel, time is moving much more slowly for the merchant than it is in, perhaps, either of the planets she is traveling to and from.

In a perfectly competitive interstellar market, the basic insight of economics is that the interest rate will equal the cost of fuel for the trip, because the net present value of the following options must be equal: (a) stay on Earth and invest in a bond and (b) buy a bond, travel at near-FTL, and multiply your earnings (since time will move faster on the planet you purchased the bond on).

Because thinking of time relativity is likely to make your head explode, a good alternative to worrying about interest rates (which no one worries about on NS much anyways) is just to adopt MT/PMT trade theory. The same principles will still be applicable, it’s just that figuring out the value of trade is much more difficult.

Bending Realism

This last section will be more of a personal reflection on the role realism in trade plays for my nation, The Macabees. I’m worried that some might interpret that there are two choices: realism and non-realism. This would be a false dichotomy, however, as the truth is that there is a spectrum. Furthermore, lying between the two poles is perfectly okay, since on NationStates it’s much, much more important to have fun than to be strictly realistic.

An example of this is financial trade between Haishan and The Macabees, two countries with considerable distance between each other. I RP as having a significant share of the financial market in Haishan (~30 percent), even though it might make more sense for another country, at a shorter distance from Haishan, to have greater access to Haize financial markets than I do. We get around this by assuming some sort of preferential treatment, and although strict realism may say that this would hurt, rather than help, our economies (more so his, perhaps), sometimes it’s just worthwhile to loosen the constraints of realism — otherwise, maybe Haishan and I would never interact, and that just wouldn’t be fun.

Another example of sacrificing realism is GATA. I created this organization to promote low-earth orbit transportation of goods, to reduce distances and transportation costs. The technologies involved may be somewhat wanked, but they’re also fun to roleplay. Of course, one has to apply reasonable discretion when choosing where to use said technology. Using wanked low-earth orbit flight in a war thread may disgruntle the other players involved, so I choose not to use it there.

This reminds me of those movies where the hero has a last-minute weapon that wins the fight and the viewer is left confused because the hero could have pulled out that weapon at any time. Well, using the weapon earlier would have ruined the plot (the fun) — a similar logic applies to NationStates.

But, there are ways to have fun while applying realism in trade. In my roleplay with Scandinvans, I’ve applied to the Alchian-Allen Theorem to describe the slave trade between Gholgoth and Theohuanacu pirates. Realism dictates that higher valued slaves are more likely to be traded with Scandinvans than lower-quality slaves, because of the high transportation costs involved. Personally, applying realism in this case makes the roleplay more interesting, because it describes a fact that not many people think about. It also bears reminding that, as an economist, I find the realism of economics fun, whereas others may not share my passion.

How realistic should you be? There’s no one answer to that. The choice is really up to you, constrained by the fact that others may choose not to interact with you if they don’t like your selective application of realism. In any case, the bottom line on NationStates is to always have fun.

_____________________

Notes:

(1) For an excellent book on German interwar economics see A. Tooze, The Wages of Destruction (New York: Viking, 2006).

(2) One of the best resources on trade theory is P. Krugman, M. Obstfeld, and M. Melitz, International Economics: Theory & Policy (Boston: Addison Wesley, 2012). The photographed graphs belong to this book.